Firestorm’s Series B

Firestorm's $82 Million Bet: How A San Diego Startup Is Reimagining Where Drones Come From

Industrial Base Alpha now offers institutional defense market research and intelligence services for investors, acquirers, and corporate strategy teams. If you need public market context, sector comps, or procurement-informed analysis to support investment and acquisition decisions, we'd like to hear from you. Fill out this short Google form to start a conversation.

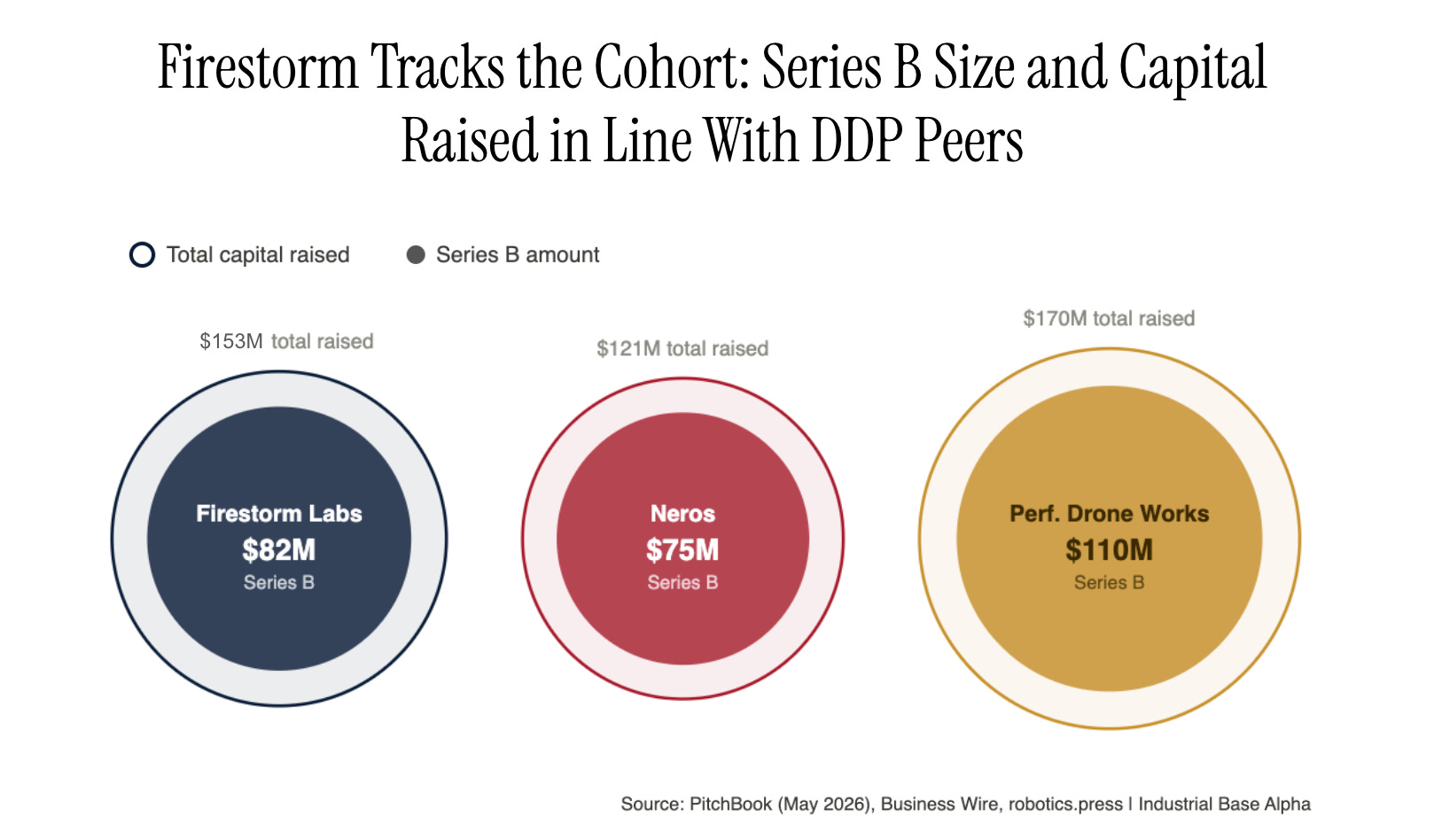

BLUF: Firestorm Labs closed an $82 million Series B on April 29, bringing total capital raised to $131.5 million and cementing its position as one of three serious contenders in the Defense Department's expeditionary drone manufacturing cohort. The round is well-structured — three tranches, a tighter syndicate led by Washington Harbour, and In-Q-Tel's first appearance as a signal that xCell has cleared classified program review. Against its DDP peers, Firestorm sits at the median on capital raised and round size, but leads the cohort on contract documentation depth, with over $25 million in confirmed 2025 revenue and a SBIR Phase III IDIQ that functions as a standing procurement vehicle for any federal agency.

On April 29, Firestorm Labs closed an $82 million Series B (shoutout to Tech Crunch for an incredible write up).

Washington Harbour led. In-Q-Tel came in for the first time. Lockheed Martin Ventures and Booz Allen Ventures followed on.

The round brings Firestorm’s total capital raised to $153 million in less than two years of serious fundraising which is a trajectory that puts it squarely inside the most competitive cohort in defense venture right now.

So what exactly does $153 million buy?

Not a drone company but a factory company. According to Dan Magy in this recent interview Firestorm Labs is shifting from being a traditional drone company to becoming a “manufacturing company that has a drone problem.”

Importantly, drones and autonomy isn’t one of the six critical technologies, while contested logistics is so this positioning and capability places Firestorm squarely in this priority where other drone companies sit on the outside.

I also note this because while I came up with some great information about how Firestorm compares relative to other industry peers who have raised a Series B, it is not a clean direct comparison.

Make your way to Industrial Base Alpha’s main website to track the latest deals, webinars, jobs, and community events.

The Factory Is the Product

The U.S. military’s drone problem is routinely described as a quantity problem. Firestorm believes it’s a logistics problem wearing a quantity problem’s clothes.

The Pentagon can identify the drones it needs. It can fund them, contract them, and in some cases field them. What it cannot reliably do is get them to the right place at the right time when the supply chain between San Diego and a forward operating location runs through ports, depots, and intermediary nodes that an adversary can target.

Firestorm’s answer is xCell: a containerized manufacturing platform that can produce drone systems in under 24 hours at the point of need. One xCell unit consists of two standard 20’shipping containers. It can be configured to produce surveillance platforms, electronic warfare systems, or lethal one-way attack drones depending on mission requirements. It can also produce replacement parts for legacy systems. The Army has already used one to print components for a Bradley Fighting Vehicle on-site. These are parts that would have otherwise taken months to arrive through conventional supply chains.

Two xCell units are currently deployed domestically — one with the Air Force Research Laboratory in Rome, New York, and one with Air Force Special Operations Command in Florida. A third is operational in the Indo-Pacific, having just completed exercise Balikatan 2026.

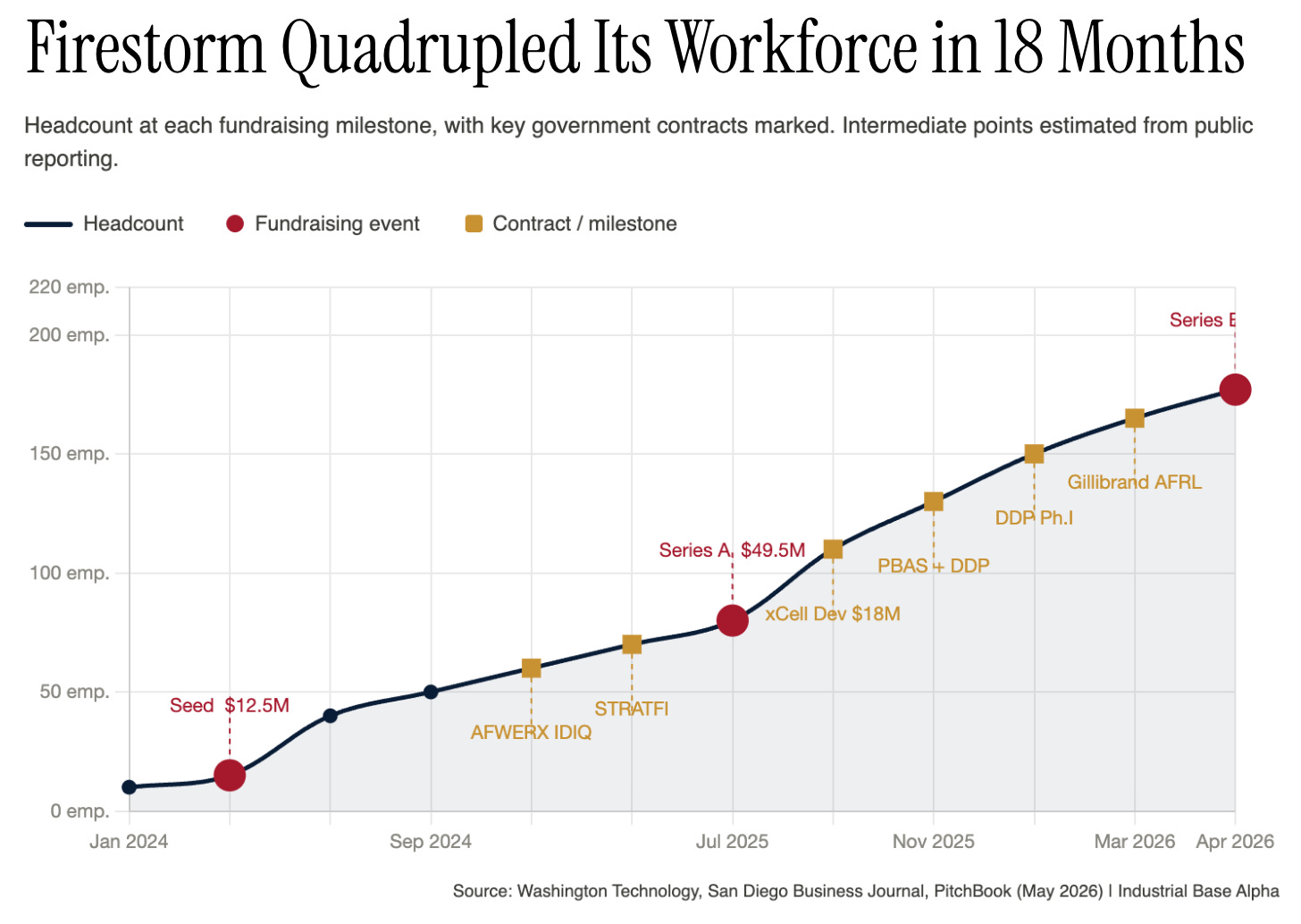

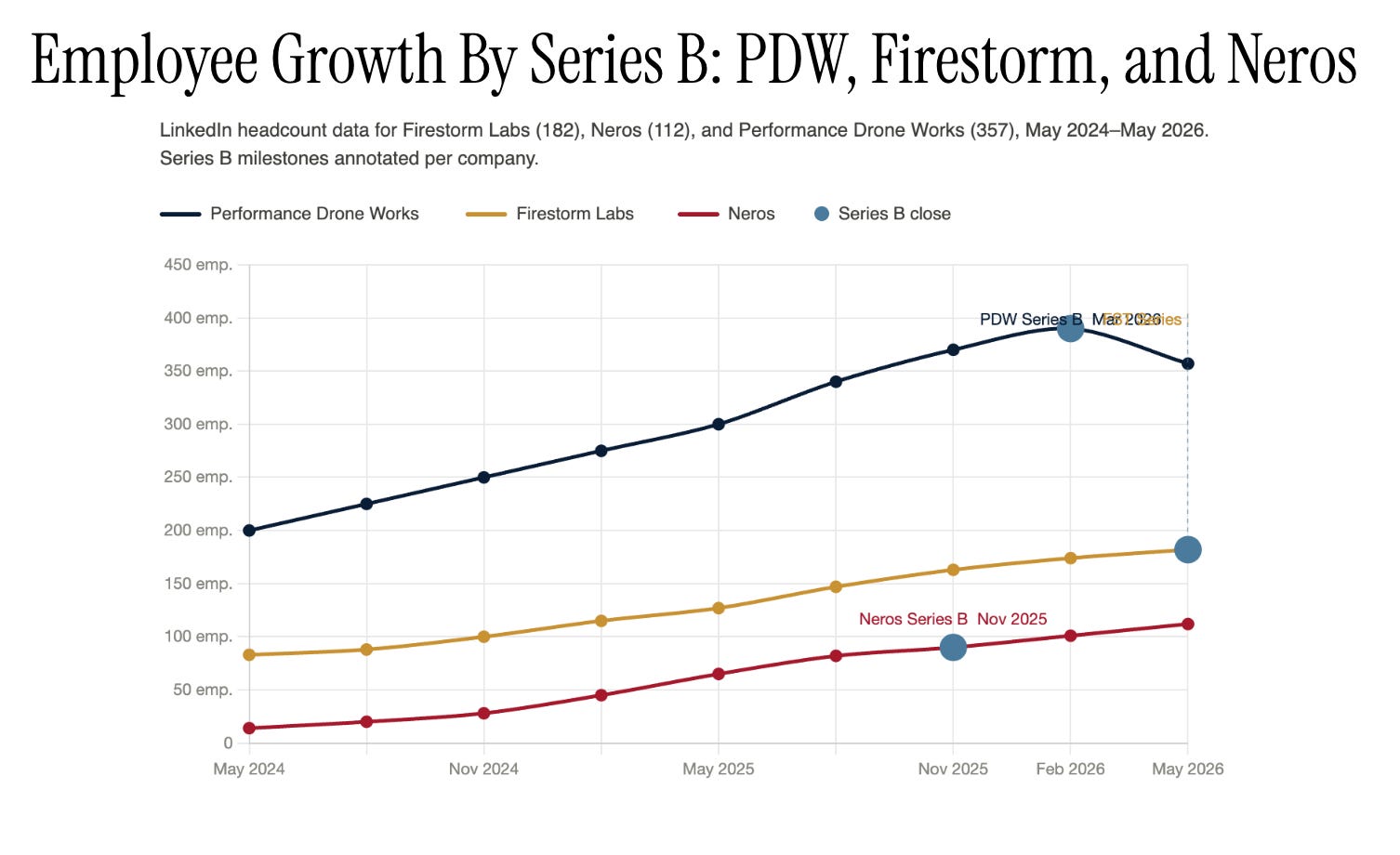

The company was founded in 2022 by Daniel Magy and Ian Muceus, both with manufacturing and aerospace backgrounds. They were joined by third co-founder Chad McCoy, a former Air Force Tier 1 Special Operator with 24 years of experience employing the very systems Firestorm makes. It went through the San Diego CONNECT accelerator in 2024, raised a $12.5 million seed, and then scaled aggressively: from roughly 40 employees at seed to 177 at the Series B close. That is a 4x headcount ramp in under 18 months, and it is faster than any comparable company in the DDP cohort.

To get a sense for how this valuation compares to other venture backed drone companies, I looked at Performance Drone Works and Neros Technologies based on their comparative technology and maturity.

Neros and the Gauntlet

In November 2025, Neros closed a $75 million Series B led by Sequoia Capital. Three months later, it placed inside the DDP top 11.

The Army’s Purpose-Built Attritable Systems program named it a primary supplier. The Marine Corps placed a large purchase order. Thousands of Archer and Archer Strike units shipped to Ukraine and to U.S. forces before the Series B closed.

Phase I placed $150 million in prototype delivery orders across 12 vendors in March 2026, with unit prices targeting $5,000 per one-way attack drone. A top 11 placement means obligated dollars on a delivery schedule. It means the Pentagon has reviewed the platform, run it through a gauntlet evaluation, and written a check.

Firestorm and PDW were both selected among the 25 DDP Phase I participants. Neither placed in the top 11.

That is not a disqualifying result. The DDP gauntlet is a platform performance evaluation. And from what I understand, Firestorm placed above average in the actual platform performance evaluation. However the DDP it measures the drone, not the factory. Firestorm is not competing to build the best drone in a gauntlet. It is competing to make the question of where drones get built a tactical decision rather than a procurement one. Those are different competitions.

But Neros won the one that produces near-term obligated revenue. And what is even more impressive is that Neros is by far the smallest and newest of these three companies.

Performance Drone Works

Performance Drone Works raised $110 million at Series B in March 2026. It opened a 90,000 square foot factory in Huntsville in August 2025. It claims annual production capacity of up to 100,000 NDAA-compliant units. On paper, PDW has the most aggressive production story in the cohort.

The complication is procurement structure. PDW’s anchor contracts are a $20.9 million Army Transformation in Contact award and an Air Force C100 contract with no disclosed value. Both are direct awards. Neither is a standing multi-agency vehicle.

Compare this to Firestorm’s $100 million AFWERX IDIQ which is structured as a SBIR Phase III contract. That means any federal agency can place orders against it without running a new competition. The ceiling is $100 million with $27 million obligated. PDW has no disclosed equivalent.

PDW also carries an implied valuation of approximately $1.2 billion based on secondary market data from Ondas Holdings’ investment. That figure has moderate confidence. If accurate, PDW is pricing at roughly 7x capital raised. Firestorm’s PitchBook estimate of $229 million implies approximately 1.7x

Quick note: From what I understand talking to insiders, this is far below the real valuation. But its what is the public’s buest guess based on Pitchbook’s algo.

The market is assigning PDW a significant premium for its factory scale and production capacity claims. Whether that premium survives the gap between claimed capacity and confirmed contract volume is worth keeping an eye on.

Reconstruction of Revenue

Big disclaimer up front: This section on approximate revenue is where there are the most gaps in public data and my numbers are surely inaccurate. But I do believe they are directionally correct and highlight the relative financial performance of these three companies to date. But take it all with a massive grain of salt.

Of the three companies, Firestorm has the most legible public contract record. The AFWERX IDIQ carries a $100 million ceiling with $27 million confirmed as obligated. The $18 million xCell System Development contract is a firm award. Add the STRATFI and DDP Phase I participation and the reconstructable obligated base sits at roughly $45 million. One LP-facing document from IPO CLUB states Firestorm’s revenue exceeded $25 million in 2025; the only disclosed revenue figure across the entire cohort. If accurate, it suggests the company was already converting government contracts into recognized revenue before the Series B closed. That is a meaningfully different risk profile than a company raising on contract ceilings alone.

PDW’s public record is thinner than its fundraising story implies. The Army Transformation in Contact award of $20.9 million is confirmed. The Air Force C100 contract exists but carries no disclosed value. Total reconstructable obligated value for PDW sits somewhere between $25 and $35 million: less than Firestorm despite a larger Series B and a more aggressive production capacity narrative. PDW’s implied $1.2 billion valuation is being underwritten primarily on factory scale and capacity claims rather than confirmed contract volume.

Neros is the hardest to reconstruct. The Army PBAS selection as a primary supplier is confirmed, but the dollar value of Neros’s share of that award has not been disclosed. The USMC purchase order exists but carries no public figure. Ukraine and allied nation deliveries — which appear to represent a meaningful portion of Neros’s actual revenue — are not U.S. government procurement instruments and do not appear in any federal spending database (emdashes human approved). The SBIR record shows early-stage DAF engagement, likely under $2 million. Confirmed U.S. government obligated value for Neros is probably under $15 million from public sources, though actual revenue is almost certainly higher and simply not visible. The DDP top 11 placement will change this picture (those delivery orders will eventually appear in FPDS) but that data is not yet public.

The Verdict

Firestorm’s Series B is a solid raise. The round size sits at the median of its DDP cohort peers, the syndicate is tighter and more strategic than the Series A, and the company is generating revenue against its contracts For a two-year-old company, that is a strong foundation.

The advanced manufacturing positioning is the most interesting part of this story. A pure-play drone manufacturer competes on platform performance and unit economics. Firestorm competes on where production happens and how fast it can be stood up. The Bradley parts use case is fantastic capability story that can help Firestorm break the narrative that they are just a drone company. And it is the kind of capability that gets pulled into programs of record organically as operators discover what the factory can do. That flexibility has long-term value that a gauntlet placement does not fully capture.

However, here is my straight foward take on the doctrinal risk: The U.S. military buys platforms. It trains on them, maintains them, and replaces them through established procurement channels. Firestorm is asking the force to do something different: to build and operate, closer to the point of need, on a shorter cycle. That is not an impossible ask, but it is a change management problem as much as a technology problem, and it will take time to work through the institutional resistance. The company is almost certainly aware of this. It is worth tracking as the DoD relationship matures.

On valuation, the honest answer is that the data is incomplete. PitchBook estimates the post-Series B value at roughly $230 million, but that figure is a model output anchored to the Series A post-money with no disclosed pre-money at B to validate it. Conversations with insiders suggest the number is reasonable and tracks the peer group — a valuation Firestorm can grow into rather than one it needs to justify immediately.

In an environment where defense tech valuations are moving quickly, the absence of a disclosed figure is frustrating but not alarming. What the public record does show is a company with real contracts, real revenue, and a capital structure that reflects genuine investor conviction.

That is enough to work with. Good job to the team at Firestorm.

Industrial Base Alpha is published by Industrial Base Alpha LLC and provides general market research, analysis, and commentary on the defense industrial base. IBA is not a registered investment adviser and does not provide investment advice. Nothing in this publication constitutes a recommendation to buy, sell, or hold any security, nor does it address the specific financial circumstances of any reader. All analysis reflects the author's views as of the date of publication and is subject to change without notice. Readers should conduct their own due diligence and consult a qualified financial adviser before making any investment decision. For full terms, see industrialbasealpha.com.

Awesome piece.

FWIW, Neros won a ~$17M contract with the USMC to deliver ~8,000 Archer Strike sUAS in November. PBAS also has an FY26 budget of over $36M, so as one of three companies under that program, Neros' revenue is likely higher than publicly disclosed, assuming orders have been placed against that. Plus, they placed second (first among US manufacturers) in DDP Gauntlet 1, which could convert into added revenue if that success continues and orders (currently listed at ~2,400) ramp up. Anecdotal, but Neros' factory (the one prior to the 250,000-square-foot Project Millennium facility) was the busiest I've visited.

Agree on Firestorms' distributed manufacturing as a core differentiator and real revenue driver (including the $30M APFIT contract—boostable to $50M—announced last week: https://www.tectonicdefense.com/exclusive-firestorm-snags-30m-apfit-contract/). That is filling a real need and delivering a critical capability, especially in INDOPACOM.

That said, Firestorm licensing HP's 3D printing technology (five-year global exclusive for use in mobile deployment units) does raise the question of what happens when that expires in ~2030 tbh—if I were HP and saw 3D-printer-based distributed manufacturing taking off, I'd think about launching my own xCell-style unit to own, manufacture, and deliver the full stack.

PDW, as far as I know, is pretty much as described. Not making the cut for DDP Gauntlet 1 is also a concern for the company, though capacity, especially relative to other firms, does matter to some degree. However, Neros can also claim that as Project Millennium comes online.